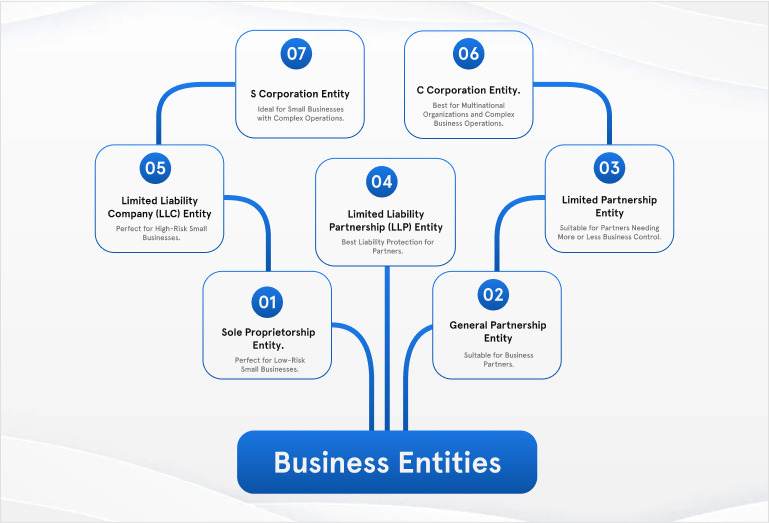

Here’s a comparison chart that outlines the key aspects of different entity types regarding ownership, tax treatment, liability protection, and tax filing requirements:

| Entity Type | Ownership | Tax Treatment | Liability Protection | Tax Filing |

|---|---|---|---|---|

| Sole Proprietorship | Single owner | Income and losses reported on owner’s personal tax return; subject to self-employment taxes | None | Schedule C with personal tax return |

| Partnership | Two or more individuals | Pass-through taxation; profits/losses reported on partners’ personal tax returns | Limited for LP and LLP, None for GP | Form 1065 (Informational) |

| Limited Liability Company (LLC) | One or more members | Default pass-through taxation; can elect to be taxed as a corporation | Limited liability for members | Default as pass-through or Form 1120/1120S if elected as corporation |

| C Corporation | Shareholders | Subject to corporate income tax; double taxation on dividends | Limited liability for shareholders | Form 1120 |

| S Corporation | Shareholders | Pass-through taxation; avoids double taxation, income/losses reported on shareholders’ personal tax returns | Limited liability for shareholders | Form 1120S (Informational) |

| Nonprofit Organization | Members/Board | Exempt from federal income taxes; must file Form 990 annually | Varies; generally limited liability | Form 990 |

This chart provides a straightforward comparison to help understand the differences between each entity type, especially in terms of how they’re taxed, the liability protection they offer, and the specific forms needed for tax filing.